Global Transport and Logistics Market Update - Week 8/2025

1. Global Container Freight Index Trends

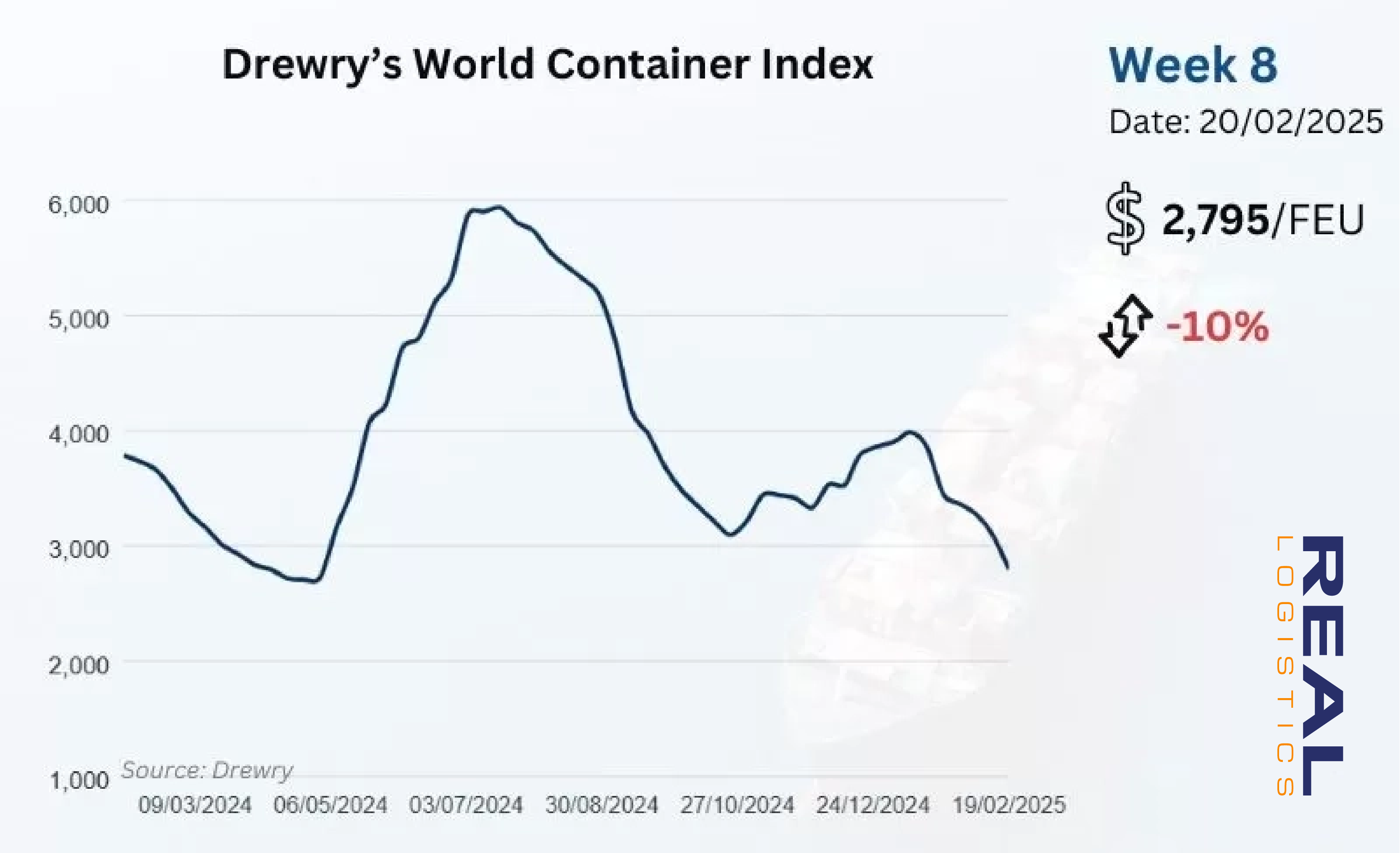

This article follows our previous analysis on container freight rates in Week 48/2024. In Week 8/2025, the Drewry Composite Container Freight Index continued its sharp decline, dropping by 10% to $2,795 per FEU. Despite this decrease, rates remain 97% higher than the pre-pandemic 2019 average of $1,420 per FEU. The downward trend reflects ongoing weak demand following the Lunar New Year holiday, coupled with excess capacity, making it difficult for carriers to maintain stable pricing.

2. Asia-North America Trade Route

Freight rates from Asia to the U.S. West Coast saw a steep decline, falling 16.10% from the previous week to $4,111 per FEU. This marks a 21.05% drop compared to last month, according to Xeneta data.

Although shipping demand is beginning to recover, it has not yet returned to pre-holiday levels. Vessel capacity has rebounded quickly, now exceeding 90%, creating an oversupply situation that continues to put downward pressure on rates.

Spot rates are still falling and may continue to decline into March unless demand picks up significantly. The likelihood of carriers implementing a General Rate Increase (GRI) in March remains low, given current market conditions. Businesses should monitor rate trends closely and plan bookings strategically to take advantage of competitive pricing.

2.1. U.S. Tariff Updates

The U.S. trade policy landscape is evolving, with several key changes already in effect:

- A 10% tariff on Chinese imports and a 25% tariff on steel and aluminum have been implemented.

- Tariffs on imports from Canada and Mexico have been postponed.

- The U.S. is considering ending the De Minimis exemption for Chinese goods, which would significantly impact low-value shipments.

- Additional trade measures under discussion include potential higher auto tariffs on Canadian vehicles and new tariffs on EU imports.

These changes could have a significant impact on global trade and supply chains, requiring businesses to reassess their sourcing strategies and seek expert logistics support to mitigate risks.

Read more:

U.S. Trade Policy 2025 - Key Measures and Implications

Tariffs Could Push Trans-Pacific Container Rates 2025

2.2. Long Beach Port Shatters January Container Volume Record

The Port of Long Beach achieved a record-breaking container volume in January, fueled by retailers accelerating imports to preempt anticipated tariffs on goods from China, Mexico, and Canada. The port processed an impressive 952,733 TEUs, a substantial 41.4% jump compared to the same period last year, and exceeding the previous January high set in 2022. Imports led the surge, climbing 45% to 471,649 TEUs, while exports saw a more modest 14% rise to 98,655 TEUs. The movement of empty containers also increased significantly, up 45.9%. This January's performance marks the eighth consecutive month of year-over-year growth for the port, following a record-setting 9.65 million TEUs handled throughout 2024.

3. Asia-Europe Trade Route

Freight rates from Asia to Northern Europe continued their sharp decline, dropping 10.80% from the previous week to $2,800 per FEU. Compared to last month, rates have plummeted by 34.40%, according to Xeneta data.

Post-Lunar New Year cargo recovery remains slow. With vessel capacity rebounding quickly, the supply-demand imbalance has led to significant downward pressure on rates.

To curb further rate declines, several carriers have announced blank sailings to limit excess capacity. Some members of the Gemini and Ocean alliances have also proposed GRIs of over 50% in March to create an upward pricing effect. However, given current market conditions, these planned increases may not materialize fully.

Businesses should consider securing bookings in February to lock in lower rates and ensure space availability, avoiding potential rate hikes in March.

4. North America-Asia Trade Route

Freight rates from North America (West Coast) to Asia fell by 1.70% week-over-week, reaching $636 per FEU. This represents a 5.22% decrease compared to last month. The decline indicates continued weak import demand in Asia post-Lunar New Year. If demand does not recover soon, further rate reductions are expected in the coming weeks.

5. North Europe-Asia Trade Route

In contrast to the downward trend on other routes, freight rates from Northern Europe to Asia saw a slight increase of 1.62% from the previous week, reaching $251 per FEU. However, rates remain 14.33% lower than last month.

This minor uptick could be attributed to carriers adjusting pricing strategies and managing capacity. However, the increase is not yet strong enough to indicate a sustained recovery.

6. Conclusion

The global ocean freight market continues to face strong downward pressure due to excess vessel capacity and sluggish demand post-Lunar New Year. Meanwhile, new U.S. tariff measures may reshape global trade flows, impacting shipping costs and import strategies for businesses.

To mitigate risks and optimize logistics costs, importers and exporters should:

- Closely monitor freight rate trends and trade policy changes.

- Book early to secure lower rates and maintain stable shipping schedules.

- Partner with professional logistics providers like Real Logistics to enhance supply chain efficiency and cost management.

📞 Contact Real Logistics today for expert consultation on international shipping and supply chain optimization!

—————————————

Real Logistics Co.,Ltd

👉 Facebook: Real Logistics Co.,Ltd

☎️ Hotline: 028.3636.3888 | 0936.386.352

📩 Email: info@reallogistics.vn | han@reallogistics.vn

🏡 Address: 39 - 41 B4, An Loi Dong, Thu Duc, HCM City

51 Quan Nhan, Nhan Chinh, Thanh Xuan, Ha Noi City